Key Finding

|

|

|

|

Introduction

Donald Trump’s defeat and Joe Biden’s victory in the 2021 US election has been hailed on both sides of the Atlantic as an occasion to restore and modernize the transatlantic alliance. Both European and American officials have listed health, trade, technology, and climate change, among other things, as new focus areas for this renewed partnership.[1] Among the myriad issues that could be tackled, the White House has sought to focus its attention first and foremost on corporate taxation.

On 1 July, 130 countries and jurisdictions joined a new framework under the OECD on international tax reform;[2] a development that follows the non-binding agreement at the G7 finance leaders meeting for a global minimum 15 percent corporate tax – something British Chancellor of the Exchequer Rishi Sunak called a “historic agreement”. [3] Both agreements suggest things are moving in the right direction. However, despite official pronouncements in international forums, European resistance towards this prospective deal on a global minimum corporation tax rate and its implementation, might scuttle ambitions for truly transformative reform. The fact that the British government sought and secured an exemption for the financial sector before the agreement was made with the OECD might be just the beginning of a broader systematic attempt to undercut it.[4]

The Biden administration is on a mission to correct a worsening historical trend in tax avoidance. The preceding decades have seen two transatlantic symbiotic trends in this domain that have allowed tax competition and avoidance to reach extreme levels, setting a terrible example globally: The systemic abuse of tax loopholes by American multinational companies and the abetting of these practices by European governments. These two dynamics have enabled a race to the bottom in effective corporate tax rates that has resulted in widespread base erosion and profit shifting.

This has led to many EU states purposefully restructuring their tax systems as offshore tax havens for US multinational corporations. This trend has reached a level where both the US and Europe are facilitating mutual tax base erosion, weakening their respective public finances and weakening the principle of mutual cooperation in tax and economic matters. Yet both the US and Europe are convinced they are being cheated by the other. The US believes Europe is allowing its companies to avoid tax altogether. The EU, on the other hand, believes the US is blocking efforts to tax American companies where they realize their profits.

The figures around tax avoidance are stark. Economists at the IMF have estimated lost revenues from tax avoidance to be as high as $650 billion annually.[5] According to data published by the OECD in 2020, multinational corporations are shifting $1.38 trillion worth of profit into tax havens.[6] The IMF has also estimated that almost 40 percent of reported cross-border corporate investment is “phantom,” meaning it is a product of accounting tricks to avoid taxation.[7] It is vital to understand that this phenomenon is not the result of underhand tax havens in far off jurisdictions, but that it takes place with the tacit support of the United States government and the European Union and its member states.

The White House believes there is an opportunity for change. On the face of it, there is apparent symmetry between the Biden administration, the EU and the UK, which have all embraced ambitious infrastructure and green transition agendas as the key metrics of political success. This requires investments at home and a levelling of the international playing field. Distortion of economic competition through tax, subsidies, and other means, are an obstacle to that central agenda. There is also domestic pressure that makes taxation a priority. In Washington, because most policy initiatives must be voted through a procedure known as “budget reconciliation” to pass the floor of the Senate, expenditure measures and investments will have to be funded completely beyond a ten-year budget horizon. In other words, no budget reconciliation bill can have a negative net revenue impact in any year beyond that point.

But there is also considerable resistance, both domestically and abroad, and vested interests that want to maintain the status quo. What’s more, the United States is in danger of misreading the European situation. While the French and German finance ministers and leaders of the European Institutions smooth things over with warm words, the EU is not in fact united on this issue and remains fearful of exposing internal rifts on the international stage. France and Germany, which are – at least on paper – the most supportive countries have been timid about the reforms. Indeed, neither the French nor the Germans put out a national official statement in support of the US’s initial proposal to establish a minimum 21 percent tax on foreign profits of US firms. In fact, German Finance Minister Olaf Scholz said, in a long bilateral Die Zeit/Le Figaro interview: “personally, I have nothing against the U.S. proposal” and France’s Bruno Lemaire conceded that “If that is the result of negotiations, we would also be agreed”. Both remarks fall some way short of unequivocal support for the US proposal and highlight the tension within Europe on this matter.[8]

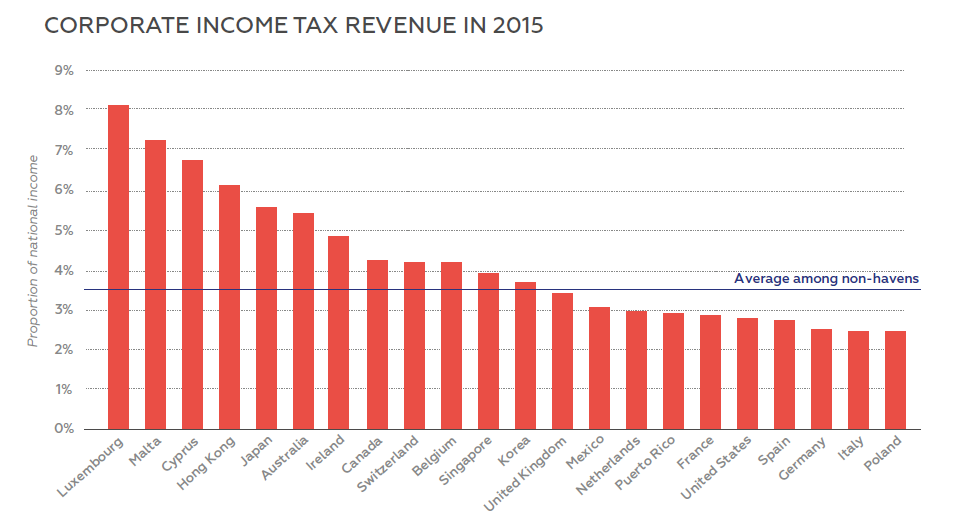

Indeed, EU member states have taken advantage of the aggressive tax competition landscape that previous US administrations have kindled around the world and have gained not only higher corporate tax revenues as a percentage of GDP, but also more innovation and employment for citizens. Among the countries that have benefited most are Ireland, which has a corporation tax rate of 12.5 percent, and Hungary, which has a corporate tax rate of 9 percent. But other countries such as Malta, Luxembourg and the Netherlands, which may officially have higher headline corporate tax rates, still benefit because they offer complex tax schemes for international companies that offset those higher rates of tax. France and Germany, as two countries that stand to gain meaningfully from reform, have only been tepid supporters and have shied away from supporting it explicitly. As a result, many countries are leading rear-guard battles in favor of the status quo, while others pay lip service to the idea of an ambitious reform.

When dealing with the EU on the issue of tax reform, the Biden administration should realize that behind the veil of support at the G7, G20 or the OECD, European countries are divided on the issue and many nations view tax competition as a central element of their strategic economic interest. Even small countries like Ireland, Malta, Bulgaria or Hungary, with a record of poor cooperation on tax matters and a willingness to wield their veto power, have the potential to unravel a deal inside the EU given that fiscal matters are decided based on unanimous votes by all member states.

Both Poland and Hungary have already called for a clause to allow domestic businesses to “opt-out” of the deal.[9] And it was a warning sign that Irish Finance Minister Paschal Donohoe, who attended the G7 as the president of the Eurogroup, only “took note” of the G7 agreement and reminded everyone that for the agreement to hold, it would need to be approved by all 139 Members of the OECD’s inclusive framework. Things became heated when Ireland, Estonia, and Hungary, joined six other states in opposing the OECD agreement in July 2021.[10] Donohoe has said that Ireland will “continue to negotiate” up until the OECD’s October 2021 deadline for finalizing the technical details and implementation plan.[11] It is in this context that the Biden’s administration’s goal of achieving international reform should be evaluated.

Following the G7 and OECD’s agreement, the United States will have to develop a much more assertive strategy and, if necessary, coercive plans for implementation if it wants to avoid its agenda being buried in EU politics. In this report, we argue that the Biden administration should not underestimate its own power, but also not expect an easy ride. We see an important precedent in the 2010 Foreign Accounts Tax Compliance Act (FATCA), which led to deep and meaningful changes on bank secrecy and the sharing of tax information within the EU. This precedent suggests, we argue, that the US can proceed with force without a final OECD deal and still manage to reshape the global taxation system.

To make this a reality, the US will need to mobilize allies so that a deal could still be implemented even if some parties do not agree to it. Indeed the US, France, Germany and a small coalition of states could unilaterally adopt a higher taxation rate for the international revenues of their companies than the one agreed at the OECD. The US’s new policy outlook towards Europe will be tested with this first bold proposal, which will require both a combination of good-spirited cooperation and effective coercive actions. Otherwise, the US risks a failure it can ill-afford to make.

OECD Negotiations: The Story so Far

Since 2013, the OECD and G20 countries have created an inclusive framework, including 139 countries, to discuss and negotiate an agreement on international taxation. The first action plan in 2015 – BEPS (Base Erosion and Profit Shifting) – saw members agree to 15 areas of cooperation but fell short of its initial ambitions due to a combination of European resistance, American corporate lobbying, and disagreements from developing nations.[12] As a result, tax avoidance techniques sprung back in different forms, and multinational company profit shifting has intensified since then.

Presently, the OECD’s efforts are focused on addressing two problems:

- Pillar I: Rethinking the allocation of taxing rights in a modern economy

Pillar I calls for rewriting profit allocation and nexus rules to give market countries taxing rights over the residual profits that multinationals make in their jurisdictions without physical presence.

- Pillar II: Ensuring that all companies pay some minimum level of tax

Pillar II calls for a minimum level of corporate taxation, primarily through a global anti-base-erosion (GlobE) mechanism comprising an income inclusion rule and the undertaxed payments rule (UTPR), which is often compared to the Global Intangible Low-Taxed Income provision, known as GILTI and the Base Erosion and Anti-Abuse Tax, known as BEAT. Both US measures set aside tranches of American corporations’ foreign income for special treatment to avoid losing tax revenue.

These OECD negotiations had previously been stymied by the United States of all parties. Under the Donald Trump presidency there was stiff US opposition both to taxing digital companies (Pillar I) and to a minimum global tax rate (Pillar II). This has left a lasting perception among other parties that the US has obstructed international tax cooperation. This has resulted in a number of European countries taking unilateral steps to tax digital companies. A new approach from Biden should have a dramatic effect on the process.

The OECD agreement in July on the two pillars above marks only the first step towards broader international tax reform. The agreement has been signed by 130 of the 139 countries under the OECD framework. Three of the countries abstaining include EU member states (Ireland, Hungary and Estonia), and the remainder are tax havens or African states. The OECD has a deadline of October 2021 to finalize technicalities and develop an implementation plan for the global minimum corporate tax rate. The coming months are therefore crucial to build consensus and create the necessary goodwill and pressure to ensure states follow through with reforms. After October 2021, states resisting the plan could either unravel the entire agreement or force a more confrontational approach between parties.

The United States’ Corporate Tax Proposal

Biden’s central policy constraint is that his plans need to pass the US Senate and therefore convince a clutch of swing US senators who care about US corporate interests in absolute terms, as well as in relation to the rest of the world. The flagship Made in America tax plan announced by the US Treasury and the White House makes progress in that direction.[13]

| Tax reform terminology: |

|---|

|

GILTI: The Global Intangible Low Tax Income is a minimum tax targeted at foreign earnings from intangible assets (copyrights, patents, trademarks, etc.). It is a way to ensure that US multinational companies pay a minimum level of tax on income earned from these assets.[14] BEAT: The Base Erosion Anti‐Abuse Tax is an additional minimum tax meant to limit the ability of corporations operating in the United States to avoid their domestic tax liability by shifting profits out of the United States. BEAT covers large corporations with gross income of over $500 million. It targets companies that have shifted over 3 percent of their total deductible payments to overseas affiliates to reduce their overall tax liability.[15] SHIELD: The Stopping Harmful Inversions and Ending Low‐Tax Developments (SHIELD) clause. This clause, proposed by the Biden Administration, would replace BEAT. It concerns payments leaving the US to countries where the effective rate is less than the US effective rate. It is intended to more effectively target perceived profit shifting to low-tax jurisdictions, while providing a strong incentive for other nations to enact global minimum tax regimes.[16] |

The domestic components of the US’s tax reform plans are fairly straight-forward. But the critical international dimension is much more complex. The central tension from the US’s perspective is that the effectiveness of this new tax rate hinges on its own ability to truly impose a new tax rate on American firms’ foreign profits.[17] This is where the problem for the US Treasury lies. As long as the tax rate in non-US jurisdictions is lower than the GILTI rate, US corporations will have an incentive to locate profits overseas or to move their company headquarters abroad, all other factors being equal.

The international dimension of the Made in America Tax Plan revolves around a few key provisions. Mostly these are about effectively targeting profit shifting to low-tax jurisdictions, while simultaneously providing a strong incentive for other nations to enact global minimum tax regimes.

One fundamental aspect of the plan, dubbed SHIELD (Stopping Harmful Inversions and Ending Low-Tax Developments), would replace the Base Erosion Anti‐Abuse Tax (BEAT) with a new regime that would deny corporate deductions on payments to foreign entities that are subject to a low effective tax rate (ETR), rather than only a low nominal tax rate. This makes an important difference and places the US in a position to adjust nominal tax rates based on US financial reporting.

The SHIELD proposal is inspired by the “undertaxed payments rule” (UTPR) in the OECD’s Pillar Two Blueprint,[18] but there are potentially significant differences underlined by a recent US Treasury presentation to the OECD Steering Group. This has substantially increased the pressure and the enforcement ability of the White House administration. Indeed, with SHIELD in place, the US could almost unilaterally impose new rules on the international revenues of US corporations while also substantially restricting transfers between US subsidiaries and their non-US based parent companies.[19] This would have the effect of substantially enhancing the US’s extraterritorial reach and could give the US the option to go it alone if OECD negotiations or implementation plans fail.

Looking forward, a critical element of the US’s ability to enforce SHIELD and effectively tax international corporations is ensuring adequate disclosure. Within the framework of its BEPS initiative, the OECD introduced a requirement for country-by-country reporting for multinational companies with revenues above €750 million per year. These reports provide data to tax authorities on the global activities and financial structure of multinationals at a country level, but are not made public.

Congress has just passed a new “Disclosure of Tax Havens and Offshoring Act” that would require public companies to disclose financial information on a country-by-country basis, including “total income tax paid on a cash basis to all tax jurisdictions.” The big difference with the OECD provisions is that this information would be public and considerably enhance the US’s ability to enforce SHIELD. The bill has not yet been voted on by the Senate and may not pass, but the Securities and Exchange Commission (SEC) could very well impose such disclosure standards through its own regulatory authority. As such, the vote of this bill in Congress increases the chances that the SEC will act independently and substantially upgrade its international tax disclosure standards. This would have profound implications for the US’s extra-territorial reach. The EU has recently passed its own corporate reporting rules that appear weaker than those currently proposed by Congress.[20]

| Country-by-Country Disclosure OECD/EU/US[21] | |||

|---|---|---|---|

| Items | OECD BEPS (Action 13) | EU public CBCR proposal | House Bill: Disclosure of Tax Havens and Offshoring Act |

| Targeted entities | Multinational Enterprises (MNEs) with a consolidated group revenue in excess of €750 million. |

Applies to:

The disclosure requirement also applies to entities, establishments, and branches:

|

Should target: “the multinational enterprise group of which the issuer is a member has annual revenue for the preceding calendar year of not less than an amount determined by the Commission to conform to United States or international standards for country-by-country reporting” |

| Is the disclosure made available to the the public | No |

Yes

The directive allows the entity concerned to defer the publication of certain figures for five years if such publication is likely to cause “significant commercial harm.” This concept is not yet defined. |

Yes |

| Total revenues | Yes – |

Yes Total revenue is defined as the sum of sales, interest income and any other accounting income in the financial statements, excluding intra-group dividends and fair value adjustments. |

No |

| Tangible assets or other than cash and cash equivalents | Yes | No | Yes |

| Number of employees |

Yes On a full-time equivalent basis. |

Yes Expressed as an annual average number of full-time employees over the year; |

Yes On a full-time equivalent basis. |

| Total accumulated earnings | Yes | Yes | Yes |

| Stated capita | Yes | No | Yes |

The European Approach

The European Union’s failure to address tax avoidance issues is profound. This failure forms the context for Biden’s new proposals. The EU’s position is one of entrenched resistance, deep disagreements, and generalized tax competition between European countries. Since 2016, the European Commission has attempted to harmonize the corporate tax bases of member states but has never attempted to harmonize corporate tax rates themselves. This is because competition and national sovereignty remains a fundamental feature of the EU when it comes to tax.

Competition between EU countries has always been viewed as legitimate policy and a natural way for small countries to improve their attractiveness. As a result, EU tax politics have been defined by a culture of resistance. National resistance has so far overcome the European Commission’s federalizing agenda. Consequently, EU negotiations have failed as member states have refused to cooperate on projects to define even the first steps towards harmonizing corporate tax rates or setting corporate tax floors.

This competitive dynamic over taxation is foundational to the EU. Indeed, since its creation, the EU’s treaties have guaranteed to EU member states that tax matters would remain issues decided based on unanimous voting. These same constitutional features have meant that workarounds have also failed. In recent years, in part because of the failure to reach a consensus on common corporate taxation, the European Commission has also tried to address the most acute tax competition problems that accrue from the individual tax rulings of member states.

In 2018, the European Commission embarked on a project to specifically tax digital services.[22] Many countries, in particular Germany, opposed the idea of progressing at the European level until an agreement could be reached via OECD negotiations. But many countries grew impatient and, eventually, a coalition of countries decided to initiate domestic digital taxes in anticipation of, and in order to weigh in on, the creation of a European piece of legislation. This has been a mixed success, both because these taxes were largely symbolic and because European momentum is still lacking. This remains an important concern of past and current US administrations and is a reason why the new Biden Administration sent a warning shot by opening and immediately closing a Section 301 investigation on Digital Services Taxes (DST).[23] This highlights that the US is prepared to put out a broad range of potentially extraterritorial and coercive measures.

Finally, the debate on the disclosure of tax-related information by corporations has become critical for the evolution of tax debates in Europe. Starting in 2017, the EU designated its own list of non-cooperative jurisdictions on tax matters, following that of the OECD in 2002.[24] Unsurprisingly, the EU list does not have any EU member states on it. But the update of the ongoing revision of the 2013 Financial Reporting Directive, is an opportunity for the EU to measure the degree of commitment to tax transparency.[25] The most recent agreement, enshrined in the so-called Country-by-Country Reporting Directive (CbCR), was agreed after five years of negotiations and only requires a partial tax disclosure for corporations.[26] Because of this directive, corporations with operations in Europe will be forced to disclose their tax payments on a country-by-country basis inside the EU and offshore jurisdictions. But for their operations in the rest of the world, corporations can present aggregate revenues.

In the face of repeated failures to make progress on tax transparency or European cooperation, and in light of the US’s renewed push to adopt tax reforms, the EU has just issued a new official communication with a new plan titled “Business Taxation for the 21st Century”.[27] To a large extent, it rehashes existing plans but tries to frame them to fit the changing international consensus. This might prove useful in changing the political balance and creating space for compromise in the EU.

If a final OECD agreement is reached on Pillar II (a minimum corporation tax rate), it will need to be transposed into EU legislation. This is both a risk for the OECD agreement and an opportunity for the EU to use this international agreement to make progress on tax issues that have been blocked for many years. While the principles of a common tax base and of formulary apportionment already featured in the previous proposal to harmonize EU corporate tax bases, the new proposal effectively builds on the momentum that the OECD agreement could provide.

That said, the EU has not entirely given up on the idea of a digital tax at the EU level and there are plans to carry this work forward irrespective of an agreement at the OECD. While the US seems to hope that a Pillar I agreement would firmly end the discussion on taxing digital companies in Europe, it may be mistaken. In fact, EU countries are questioning Washington’s demands that they roll back national taxes on technology companies once a global levy on multinational companies is agreed. Given European sensitivities around tax sovereignty, aggressive US actions on digital tax could be counterproductive.

Whether or not the US may have to rely on coercive action depends on the implementation of any OECD tax deal. National reactions to the agreement are therefore important to monitor. Indeed, while countries that are key beneficiaries of tax arbitrage and competition, such as the Netherlands, Luxembourg, or Ireland, might prove willing to cooperate, others such as Malta, Poland, and Hungary, for example, might make a stronger case for resisting implementation. The real danger for the US is that international efforts to secure a deal break down because of internal EU deadlocks. The US administration should be extremely alert to this risk because European failure to implement an OECD Pillar II agreement could empower skeptical members of congress and senators who are concerned about the competitive position of US firms.

Potential opposition amongst European countries

| Announced, Potential, and Expected Opposition to Tax Reform Plans | ||

|---|---|---|

| Countries | Countries that have taken an official stance against the agreement | Support the OECD agreement? |

| Ireland | Ireland’s Deputy Prime Minister Leo Varadkar defended the country’s 12.5 percent corporation tax rate recognizing that it represents a significant amount of revenue for the state.[28] |

No Ireland did not sign the OECD July agreement. |

| Hungary | Prime Minister Viktor Orban, on the basis of defending the economic attractiveness of his country, has expressed his opposition to the agreement: “I consider it absurd that any world organisation should assert the right to say what taxes Hungary can levy and what taxes it cannot, [...] Especially as we are not a tax haven, because the low Hungarian corporate tax rate is not meant to attract certain companies to declare their taxes here”.[29] Hungary also argues that the current proposal violates EU law.[30] |

No

Hungary did not sign the OECD July agreement. |

| Poland | Finance Minister Tadeusz Kościński did initially oppose the proposal, saying that taxes are essential for attracting investment and therefore for countries to catch up with more advanced economies.[31] But Poland changed his position after the inclusion of a carve-out for substantial business activity.[32] | Yes |

| Cyprus | The Minister of Finance Constantinos Petrides suggested that Cyprus could veto the EU adoption of the deal.[33] | Not a member |

| Estonia | Estonia has said it will challenge the translation of the agreement into European law | No |

| Countries with reservations about implementing the agreement in full | ||

| United Kingdom | The United Kingdom, although enthusiastic at the beginning, secured an exemption for financial services in the OECD July agreement after an intervention by Chancellor of the Exchequer Rishi Sunak. | Yes |

| Switzerland | There is a consultation of local governments to examine how federal subsidies might offset the effects on the Cantons should Switzerland sign the deal.[34] | Yes |

| Countries that are supportive but may backtrack as beneficiaries of the status quo or due to lobbying | ||

| Netherlands | The Netherlands has expressed publicly its desire to implement the agreement in full.[35] | Yes |

| Luxembourg | Luxembourg’s prime minister has expressed support for the agreement on social media. | Yes |

| Countries with no official position but which are expected to oppose as they benefit from the status quo | ||

| Malta | Malta has not yet taken an official stance on the question. | Not a member |

| Bulgaria | Bulgaria has not yet taken an official stance on the question. | Not a member |

Securing an Ambitious Deal

While the Biden administration has thrown its support behind global minimum taxation under Pillar II, Washington has been evading the discussion of a specific set of taxation rules for the digital economy. This is because the US, even under the Biden administration, feels that it specifically targets US corporations.

The proposal agreed at the G7 and OECD would see countries share tax revenues when companies have revenues in excess of €20 Billion per year and more than a 10 percent profit margin (pre-tax profit/sales) irrespective of the sector they operate in (Pillar I) and a minimum tax rate on countries with revenues in excess of €750 million per year (Pillar II). But this scope is problematic and liable to countless arguments. Profit margins are an easily manipulable figure and the OECD agreements will have to define the scope more precisely before the OECD’s October final agreement to mitigate manipulation. However, there is a trade-off here between the breadth of coverage and the operational limitations of any agreement. This will require negotiation for each company and each country in which they have operations. Starting with rules that impact a limited number of companies might be a reasonable first step.

The central political question of these negotiations lies with estimating the effects of these changes in terms of the redistribution of tax revenues. What is clear is that most tax havens with low nominal tax rates have been able to generate above average corporate tax revenues as a percentage of GDP. Those countries stand to lose from this proposed tax reform. The US, on the other hand, stands to recover a large amount of tax revenues lost to the EU. Therefore, its aggregate corporate tax revenues will rise. This means that even if the EU loses corporate tax to the US in relative terms, it might still gain new revenues in absolute terms due to a higher minimum corporate tax rate. The US’s proposal should not, therefore, be seen as a zero-sum game.

Calculation of the amount and distribution of new tax receipts, however, is not straight-forward. The European Tax Observatory simulator suggests that a 15 percent effective tax rate would increase the global corporate tax windfall by €120 billion. France’s Council of Economic Analysis (CAE),[36] suggests that €109 billion of global corporate tax will be recouped. One further estimate in a forthcoming analysis by Devereux and Simmler suggests that only around €73 billion will be recovered.[37] What matters greatly in the difference between these estimates is the €750 million revenue threshold for the minimum corporate tax rate to apply. This limit narrows the scope of application of the rules quite considerably and modifies the relative importance of three impact channels : (i) reallocation of production, (ii) reallocation of tax base (mostly through intangible booking) and (iii) the minimal taxation of profits in tax havens (rate effect).

Over time, it is fair to assume that tax havens would lift their tax rates to the global minimum rate and this would gradually bring the effect on public finances of taxing affiliates which still transfer profits to tax havens close to zero in the medium-term. The short-term and long-term estimates of the tax gains may therefore vary greatly.

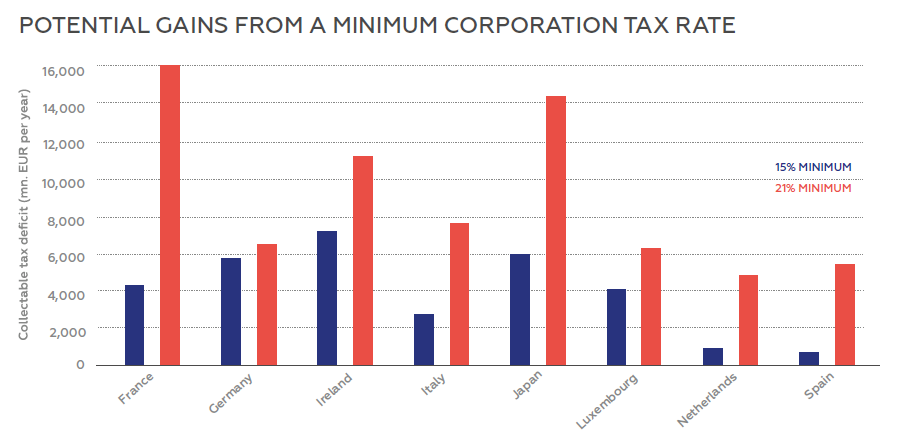

Potential Gains from a Minimum Corporation Tax Rate

|

How to compute the tax deficit This tax deficit calculation is based on the European Tax Observatory report.[38] It calculates the difference between what a company currently pays in taxes and what it would have to pay if it were subject to a minimum tax rate in each country where it operates. To estimate the tax deficit, the authors combined two datasets. The first dataset is the tabulation of multinational corporations’ country-by-country reports published by the OECD in July 2020. The second dataset is the estimates of the profits booked in tax havens by the parent country. Here are some of the assumptions made by tha authors of the report to calculate profits booked in tax havens" (i) Profits booked in tax havens by countries that report have been estimated as per the methodology in Tørsløv, T. R. et al (2018). (ii) Profits booked in tax havens by parent companies that do not report country-by-country data are assumed to be taxed at an effective tax rate of 10 percent (a rate in line with the one observed in country-by-country statistics in 2016). (iii) For profits booked in non-haven countries by parent companies that report country-by-country data, the tax deficit is estimated using the OECD data (profits and effective tax rates) with no correction. (iv) Profits booked in non-havens by parent companies that do not report country-by-country date are imputed based on the ratio of non-haven to haven tax deficits for the countries that report country-by-country data to the OECD. This estimate, contrary to others like Laffite’s, was calculated without a threshold of €750 million per year. Therefore, the tax deficit here includes all corporations in the territory whose effective rate is lower than the minimum rate. This means the estimate tends to overstate the tax deficit. But while the estimates vary, the most important effect that is hard to model is the speed at which tax havens will adjust their tax rate to that of the global minimum tax rate. Council of Economic Analysis Estimation[39] The French Council of Economic Analysis has conducted micro-economic analysis to understand the trade‐offs faced by corporations and their short‐ and medium‐term decisions. If the agreement is enacted, the consequences on tax revenues can be broken down into three effects:

The CAE estimates that up to $130 billion of profit will be redirected to countries of sale. The CAE has also concluded that a 15 percent minimum tax could raise corporate tax revenues by €8 billion, €6 billion, and €15 billion for France, Germany and the US respectively. EconPol Europe estimation[40] Finally, a study by EconPol estimates that up to $87 billion of profit will be redirected and that around 64 percent of this total ($56 billion) would be generated by US-headquartered companies. This study underlines most importantly that the decision to exclude financial companies reduces the profits redirected by around half. |

There is one significant gap in the Biden proposal. Emerging economies are an important and under-represented party to this negotiation as they stand to lose important revenues from the new agreement. Their interests must also be considered. This is the reason why some have preferred to lobby the UN’s Economic and Social Council on tax matters and flesh out an alternative proposal (the Tax Treaty, Provision on Payments for Digital Services Proposal) to the OECD’s Pillar I agreement. [41] In particular, this proposal broadens the scope considerably beyond the largest companies with the highest profit margins and focuses specifically on automated digital services (e.g. data and advertising) by allowing source countries to apply a withholding tax on these revenues.

The Tax Treaty, Provision on Payments for Digital Services , which has been adopted by the UN, is just a model document at this stage and is not enforceable, but it could fuel resistance from developing countries at the OECD. The question of the deal’s global legitimacy has been raised through the emergence of this proposal and must be addressed by the EU and the US together.

Given these complexities and uncertainties within the EU, the Biden administration should begin to develop a diplomatic plan. This plan should include potential coercive measures. But it will have the greatest chance of success if the US can enlist some willing partners in the EU that are able to pressure other member states. The United States, with a coalition of the willing, will need to use its bilateral power to pressure jurisdictions likely to block the agreement and seriously consider developing control and enforcement mechanisms to ensure swift progress.

The experience of introducing FATCA in 2009 provides some clues as to what can be done to ensure rapid implementation. Back then, the United States essentially compelled European financial institutions to share bank information about US citizens internationally, which resulted in profound changes to bank secrecy in Europe for everyone, including European citizens. Strong external pressure from the US can sometimes help overcome European domestic resistance. These efforts should be focused on the following six axes:

- Building a Coalition

The United States should establish a coalition of countries, in Europe in particular, that is willing and able to approve a more ambitious agreement than the OECD.[42] This effort should specifically target the United Kingdom, France, Germany, and Japan as the largest economies, the most like-minded countries on international issues, and countries that host some of the largest multinationals. These countries should be prepared to increase international corporate taxation on their companies to 21 percent and to implement it unilaterally. This “coalition of the willing” would effectively announce its commitment to legislate provisions along the lines of SHIELD, thereby imposing a higher corporate tax rate on its companies than the minimum agreed at the OECD. This coalition of countries could set out a timeline by which it expects the rest of the world to join the initiative. Doing so would create an impression of inevitability and add immense pressure on the outlier states to conform and harmonize. It would put coalition countries’ corporations at a temporary competitive disadvantage but would signal an overwhelming willingness to act. This might prove more challenging for European countries given the principle of non-discrimination within the EU, but there are options to work around these obstacles.[43]

- Improving Disclosure Standards and Enforcement

The information on global tax avoidance remains weak. The United States could play a central international role in forcing greater disclosure, either via legislative action as is currently underway in Congress or via the SEC’s regulatory authority. Indeed, the United States requiring country-by-country reporting of all tax payments of all companies operating in the United States would have far reaching international consequences. In the same way that the US government requires international banks to release banking information of all US citizens upon request, it should be able to require the same from US corporations. The combination of mandatory reporting and possible verification via bank information would set a global standard that would help improve the new EU disclosure standards that were recently adopted. This would also encourage parties to make the OECD’s existing country-by-country reporting public.

- Naming and Shaming

The United States should introduce a new “International Tax Situation Report” that would be put together by the US Treasury, inspired by the “Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States”. This would allow the US Treasury to call out countries engaging in currency manipulation and seek redress. This report should explicitly name and shame countries, including EU member states that hold up progress on global tax reform. They should be warned that unless they move forward on taxation issues they risk being specifically added to a new official US government list, potentially named “Corporate Tax Avoidance Enabler”.

- Using Joint Diplomatic Pressure

As the “Corporate Tax Avoidance Enabler” list is being drawn up, the White House, along with willing EU member states, should begin a series of calls with leaders involving the US president, followed up by calls from the secretary of state and the secretary of the Treasury. These calls should make clear that no movement on these issues would be seen as a diplomatic affront with consequences triggering a “crisis” in the relationship. This would encourage the willing EU countries to adopt a similar list and review/expand its own list of non-cooperative jurisdictions.

- Enforcing Diplomatic Restrictions

If no action is taken, these states should be designated “Corporate Tax Avoidance Enablers” and a series of diplomatic restrictions should be put in place. The White House should dial back access to administration officials, non-critical diplomatic support in international forums, and high profile visits. White House officials should openly talk about a “crisis” in the relationship. If necessary, the US should use its significant diplomatic presence in Europe, from ambassadors downwards, to place the pressure on these states on all levels of government to campaign for change.

- Wielding National Security Tariffs and Taxes.

The administration has already developed an expansive understanding of its national security interest. The United States has already effectively used the powers of the threat of an investigation under Section 301 – a measure that allows the president to act against discriminations against US industry. In this case, to signal its readiness to take action against unilateral digital taxation amendments. While it has so far been used to protect the interests of the US tech industry rather than improve international taxation standards, this should remain a tool the administration is prepared to use. Meanwhile, the legality of invoking national security for tax matters should remain open. A Section 232 investigation, which enables the president to act against national security threats in trade, may not pass World Trade Organization scrutiny and therefore should not be put to test, but the US administration should make clear the seriousness with which it considers the issue of tax cooperation. Leaving the threat of Section 232 investigations on the table is a great way to do that.

Conclusion

This is a decisive moment for the Biden administration. It is hard to understate the importance of this international tax deal both for the administration’s domestic economic policy outlook as well as for its global standing and ability to secure international diplomatic progress. Failure to follow through would have profound consequences on both the domestic and multilateral agenda, from climate change to alliance-maintenance.

Meanwhile, the EU is divided on this matter and is therefore both a potential strong ally as well as a source of potential obstacles. The Biden administration must be prepared to use these divisions to create peer pressure and, if necessary, use coercion tactics with uncooperative parties.

To be credible, the US must be successful in projecting its diplomatic power to secure a strong international coalition of the willing. However, it must also be prepared to act unilaterally with force to show its commitment to this cause. The precedent surrounding the implementation of FATCA shows that by doing so the United States does have the power to mold the tax environment in Europe through its actions.

This effort is an important test for transatlantic relations and it can, with some unavoidable frictions, bring Washington and Brussels closer together. If the US is successful in pushing through its agenda, it will also deliver on the European Commission’s longstanding aspiration to harmonize Europe’s tax base. Despite opposition in some European capitals, the US and the EU’s interests are fundamentally aligned.

Footnotes

[1] Secretary Antony J. Blinken and European Commission President Ursula von der Leyen (2021) ‘Secretary Antony J. Blinken and European Commission President Ursula von der Leyen Before Their Meeting Remarks to the Press’. Berlaymont Brussels, Belgium, 24 March. Available at: https://www.state.gov/secretary-antony-j-blinken-and-european-commissio… (Accessed: 29 July 2021).

[2] OECD (2021) ‘130 countries and jurisdictions join bold new framework for international tax reform’, 1 July. Available at: https://www.oecd.org/newsroom/130-countries-and-jurisdictions-join-bold-new-framework-for-international-tax-reform.htm (Accessed: 16 July 2021).

[3] Phillip Inman and Michael Savage (2021) ‘Rishi Sunak announces “historic agreement” by G7 on tax reform’, the Guardian, 5 June. Available at: http://www.theguardian.com/world/2021/jun/05/rishi-sunak-announces-hist… (Accessed: 14 June 2021).

[4] Reuters (2021) ‘UK wins financial services carve-out from new global tax rules - FT’, 30 June. Available at: https://www.reuters.com/world/uk/uk-wins-financial-services-carve-out-n… (Accessed: 8 July 2021).

[5] Kinder, T. and Agyemang, E. (2020) ‘“It’s a matter of fairness”: squeezing more tax from multinationals’, Financial Times, 8 July. Available at: https://www.ft.com/content/40cffe27-4126-43f7-9c0e-a7a24b44b9bc (Accessed: 2 June 2021).

[6] Mark Bou Mansour (2020) ‘$427bn lost to tax havens every year: landmark study reveals countries’ losses and worst offenders’, Tax Justice Network, 20 November. Available at: https://taxjustice.net/2020/11/20/427bn-lost-to-tax-havens-every-year-l… (Accessed: 14 June 2021).

[7] Damgaard, J., Elkjaer, T. and Johannesen, N. (2019) ‘Empty corporate shells in tax havens undermine tax collection in advanced, emerging market, and developing economies’, Finance & Development, 56(3), pp. 11–13.

[8] Reuters (2021) ‘German, French ministers back U.S. on 21% minimum corporate tax rate -Zeit’, 27 April. Available at: https://www.reuters.com/article/us-germany-france-tax-idUSKBN2CE0FY (Accessed: 27 July 2021).

[9] Hall, B. (2021) ‘Poland and Hungary call for domestic business opt-out from G7 tax deal’, Financial Times, 9 June. Available at: https://www.ft.com/content/318d19a6-6c7f-499e-b144-4050296a53c8 (Accessed: 14 June 2021).

[10] Euronews (2021) ‘Ireland, Hungary and Estonia opt out of OECD tax deal and cast shadow over EU’s unified position’, 2 July 2021. Available at: https://www.euronews.com/2021/07/02/ireland-hungary-and-estonia-opt-out… (Accessed: 16 July 2021).

[11]Reuters (2021) ‘Ireland fails to back global corporate tax proposal over 15% rate’, 1 July 2021. Available at: https://www.reuters.com/business/ireland-declines-back-oecd-corporate-t… (Accessed: 16 July 2021).

[12] Base Erosion and Profit Shifting Final Reports - OECD (2015). OECD. Available at: https://www.oecd.org/ctp/beps-2015-final-reports.htm (Accessed: 27 July 2021).

[13] The Made in America Tax Plan Report (2021). U.S. DEPARTMENT OF THE TREASURY. Available at: https://www.journals.uchicago.edu/doi/10.1086/703226 (Accessed: 14 June 2021).

[14]‘GILTI: Global Intangible Low Tax Income | Tax Foundation’ TAX BASICS. Available at: https://taxfoundation.org/tax-basics/global-intangible-low-tax-income-g… (Accessed: 8 July 2021)

[15] ‘Base Erosion and Anti-Abuse Tax (BEAT) | Tax Basics | Tax Foundation’ TAX BASICS. Available at: https://taxfoundation.org/tax-basics/base-erosion-anti-abuse-tax-beat/ (Accessed: 8 July 2021).

[16]Marcus Heyland, Jonathan Galin, and Danielle Rolfes (2021) U.S. Tax Reform 2.0—BEAT Down, SHIELD Up? Available at: https://news.bloombergtax.com/daily-tax-report/u-s-tax-reform-2-0-beat-… (Accessed: 8 July 2021).

[17] Huaqun Li, Garrett Watson, and Taylor LaJoie (2020) ‘President Biden’s Tax Plan: Details & Analysis’, Tax Foundation, 22 October. Available at: https://taxfoundation.org/joe-biden-tax-plan-2020/ (Accessed: 14 June 2021).

[18] Marcus Heyland, Jonathan Galin, and Danielle Rolfes (2021) ‘U.S. Tax Reform 2.0—BEAT Down, SHIELD Up?’, Bloomberg tax, 17 May. Available at: https://news.bloombergtax.com/daily-tax-report/u-s-tax-reform-2-0-beat-… (Accessed: 8 July 2021).

[19] However, several critical questions remain open: (for instance, the scope of companies covered by these rules (revenue threshold), and the deductions allowed to calculate the effective tax rate, to name two. Many of these are addressed in the Treasury Department’s annual report on the administration’s revenue proposals (commonly referred to as the “Greenbook”). General Explanations of the Administration’s Fiscal Year 2022 Revenue Proposals (2021). Department of the Treasury. Available at: https://home.treasury.gov/system/files/131/General-Explanations-FY2022….

[20] EY (2021) ‘EU co-legislators reach agreement on public CbCR’, Tax News Update U.S Edition, 2 June. Available at: https://taxnews.ey.com/news/2021-1097-eu-co-legislators-reach-agreement… (Accessed: 30 June 2021).

[21] PwC (2021) ‘EU Directive proposals would widen public country-by-country reporting’, TaxPolicy Bulletin, 11 March. Available at: https://www.pwc.com/gx/en/tax/newsletters/tax-policy-bulletin/assets/pw… (Accessed: 30 June 2021);

KPMG (2021) ‘Country by Country Reporting : An overview and comparison of initiatives’, May. Available at: https://assets.kpmg/content/dam/kpmg/xx/pdf/2021/05/kpmg-cbcr-overview-… (Accessed: 30 June 2021); EY (2021) ‘EU co-legislators reach agreement on public CbCR’, Tax News Update U.S Edition, 2 June. Available at: https://taxnews.ey.com/news/2021-1097-eu-co-legislators-reach-agreement… (Accessed: 30 June 2021).

[22] EUROPEAN COMMISSION (2018) Proposal for a COUNCIL DIRECTIVE laying down rules relating to the corporate taxation of a significant digital presence COM/2018/0147 final - 2018/072 (CNS). Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52018PC0147 (Accessed: 14 June 2021). Note that A digital service is a service that is delivered over the internet or an electronic network and the nature of which renders their supply essentially automated and involving minimal human intervention. This definition corresponds to the definition of 'electronically supplied services' in Article 7 of the Council Implementing Regulation (EU) No 282/2011 of 15 March 2011 laying down implementing measures for Directive 2006/112/EC on the common system of value added tax, and includes the same kind of services. The mere sale of goods or services facilitated by using the internet or an electronic network is not regarded as a digital service. For example, giving access (for remuneration) to a digital marketplace for buying and selling cars is a digital service, but the sale of a car itself via such a website is not.

[23] United States Trade Representative Katherine Tai (2021) USTR Announces, and Immediately Suspends, Tariffs in Section 301 Digital Services Taxes Investigations | United States Trade Representative. Office of the United States Trade Representative. Available at: https://ustr.gov/about-us/policy-offices/press-office/press-releases/20… (Accessed: 27 July 2021).

[24] Council conclusions on the revised EU list of non-cooperative jurisdictions for tax purposes 2020/C 64/03 ST/6129/2020/INIT OJ C 64, 27.2.2020, p. 8–14 (2020). Available at: https://eur-lex.europa.eu/legal-content/en/TXT/?uri=CELEX%3A52020XG0227… (Accessed: 14 June 2021).

[25] European Council and European Parliament (2013) DIRECTIVE 2013/34/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings, amending Directive 2006/43/EC of the European Parliament and of the Council and repealing Council Directives 78/660/EEC and 83/349/EEC. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32013L00… (Accessed: 8 July 2021).

[26] EY (2021) ‘EU co-legislators reach agreement on public CbCR’, Tax News Update U.S Edition, 2 June. Available at: https://taxnews.ey.com/news/2021-1097-eu-co-legislators-reach-agreement… (Accessed: 30 June 2021).

[27] EUROPEAN COMMISSION (2021) COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Business Taxation for the 21st Century.

[28] Shawn Pogatchnik (2021) ‘Ireland defends tax regime amid demands for global minimum rate’, POLITICO, 10 June. Available at: https://www.politico.eu/article/ireland-defends-tax-regime-amid-demands… (Accessed: 15 June 2021).

[29] Reuters Staff (2021b) ‘Orban says global minimum tax plan “absurd”, Hungary may look at options’, Reuters, 9 June. Available at: https://www.reuters.com/article/us-oecd-tax-hungary-idUSKCN2DL19A (Accessed: 15 June 2021).

[30] Hungary and Estonia have argued that the proposal contravene a 2006 ruling by the European Court of Justice. The ruling said basing subsidiaries of multinationals in lower tax regimes does not constitute tax avoidance

Mehreen Khan et al., “Legal Wrangle Raises Hurdles to EU Implementation of Global Tax Deal,” Financial Times, July 6, 2021, https://www.ft.com/content/e51c4a7b-a64d-40e5-b45c-e53ebdf284fe.

[31] Hall, B. (2021) ‘Poland and Hungary call for domestic business opt-out from G7 tax deal’, Financial Times, 9 June. Available at: https://www.ft.com/content/318d19a6-6c7f-499e-b144-4050296a53c8 (Accessed: 14 June 2021).

[32] Mehreen Khan et al., “Legal Wrangle Raises Hurdles to EU Implementation of Global Tax Deal,” Financial Times, July 6, 2021, https://www.ft.com/content/e51c4a7b-a64d-40e5-b45c-e53ebdf284fe.

[33] Daniel Boffey (2021) ‘Cyprus could block EU adoption of minimum corporate tax plan’, the Guardian, 3 June. Available at: http://www.theguardian.com/politics/2021/jun/03/cyprus-block-eu-adoptio… (Accessed: 15 June 2021).

[34]Sam Jones (2021) ‘Switzerland plans subsidies to offset G7 corporate tax plan’, SWI swissinfo.ch, 11 June. Available at: https://www.swissinfo.ch/eng/switzerland-plans-subsidies-to-offset-g7-c… (Accessed: 28 June 2021).

[35] Christopher Cloutier (2021) ‘Why tax haven the Netherlands says yes to the G7 agreement’, Netherlands News Live, 14 June. Available at: https://netherlandsnewslive.com/why-tax-haven-the-netherlands-says-yes-… (Accessed: 15 June 2021).

[36] Laffitte, S. et al. (2021) Taxation of Multinationals: Design and Quantification. Conseil d’Analyse Economique: CAE.

[37] Michael Devereux, Martin Simmler: "Who Will Pay Amount A?", EconPol Policy Brief 36, July 2021

[38] Mona Barake et al. (2021) Collecting the Tax Deficit of Multinational Companies: Simulations for the European Union. 1. EU Tax Observatory. Available at: https://www.taxobservatory.eu/wp-content/uploads/2021/06/TaxObservatory… (Accessed: 7 June 2021).

[39] Laffitte, Sébastien et al. 2021. “Taxation of Multinationals: Design and Quantification.”

[40] Michael Devereux, Martin Simmler: "Who Will Pay Amount A?", EconPol Policy Brief 36, July 2021.

[41] UN Committee of Experts on International Cooperation in Tax Matters (2021) Drafting Group Proposal – Possible Tax Treaty, Provision on Payments for Digital Services. Available at: https://www.un.org/development/desa/financing/sites/www.un.org.developm… (Accessed: 14 June 2021).

[42] Arturo Herrera Gutiérrez et al. (no date) ‘Opinion | Five finance ministers: Why we need a global corporate minimum tax’, Washington Post. Available at: https://www.washingtonpost.com/opinions/2021/06/09/janet-yellen-global-… (Accessed: 14 June 2021).

[43] There are essentially two avenues to work around EU law restrictions. The first and most obvious one is to apply the same tax on foreign earned income as on domestic incomes. The second is to create a specific substance based carve out that would essentially only apply to affiliates that have no real activity. Both options carry legal risks and might be challenged in court, but they are a weapon probably worth waging to force action.

Englisch J. (2021) “International Effective Minimum Taxation. Analysis of GloBE (PillarTwo)” in Handbook of International Tax Law, Haaseet Kofler (eds), Oxford University Press (OUP), forthcoming.